Grain market outlook - August 2012

Author: Lachie Stevens | Date: 29 Aug 2012

Lachie Stevens,

Lachstock Consulting

Keywords: grain market, supply, demand, marketing

Take Home Messages:

- Final results of US drought will have a strong impact on the market

- Demand changes will be dependent on ultimate world supply

- A lot can and will change in the coming 12 month marketing window.

- Be objective and realistic about your targets.

- Measure Risk vs. Reward and only hedge when the risk and reward warrants it and don’t look a gift horse in the mouth.

- Be consistent with your plan and maintain a disciplined approach.

Introduction

- Bachelor of Agricultural Science - Melbourne University

- Risk Management and Marketing - Monash University

- Advance Graduate Diploma of Applied Finance and Investment – FINSIA

- Louis Dreyfus (2001 - 2007)

–Analyst, Oilseed trader, Wool trader, Sorghum trader and Risk manager.

- Lachstock Consulting (2007 - Present)

–Grain and Dairy Farm Advisory Services

–Daily and Weekly Grain Market Reporting Services

–Advice to Grain and Dairy Corporate Clients

- XLD Grain (2010 - Present)

–Grain trading and storage organisation servicing Tasmanian grain producers and consumers

Market Overview

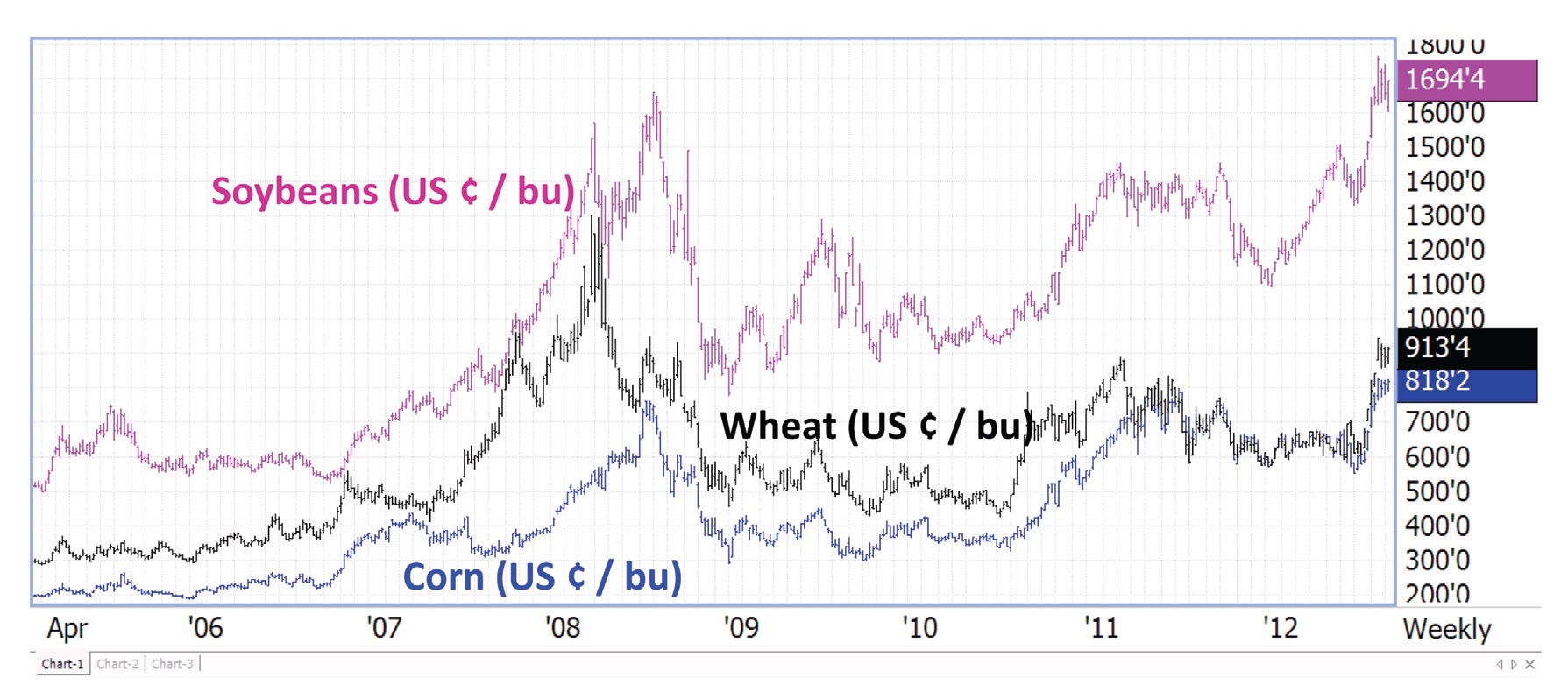

Figure 1. Recent US corn, wheat, and soybean price history (Data source: Future markets)

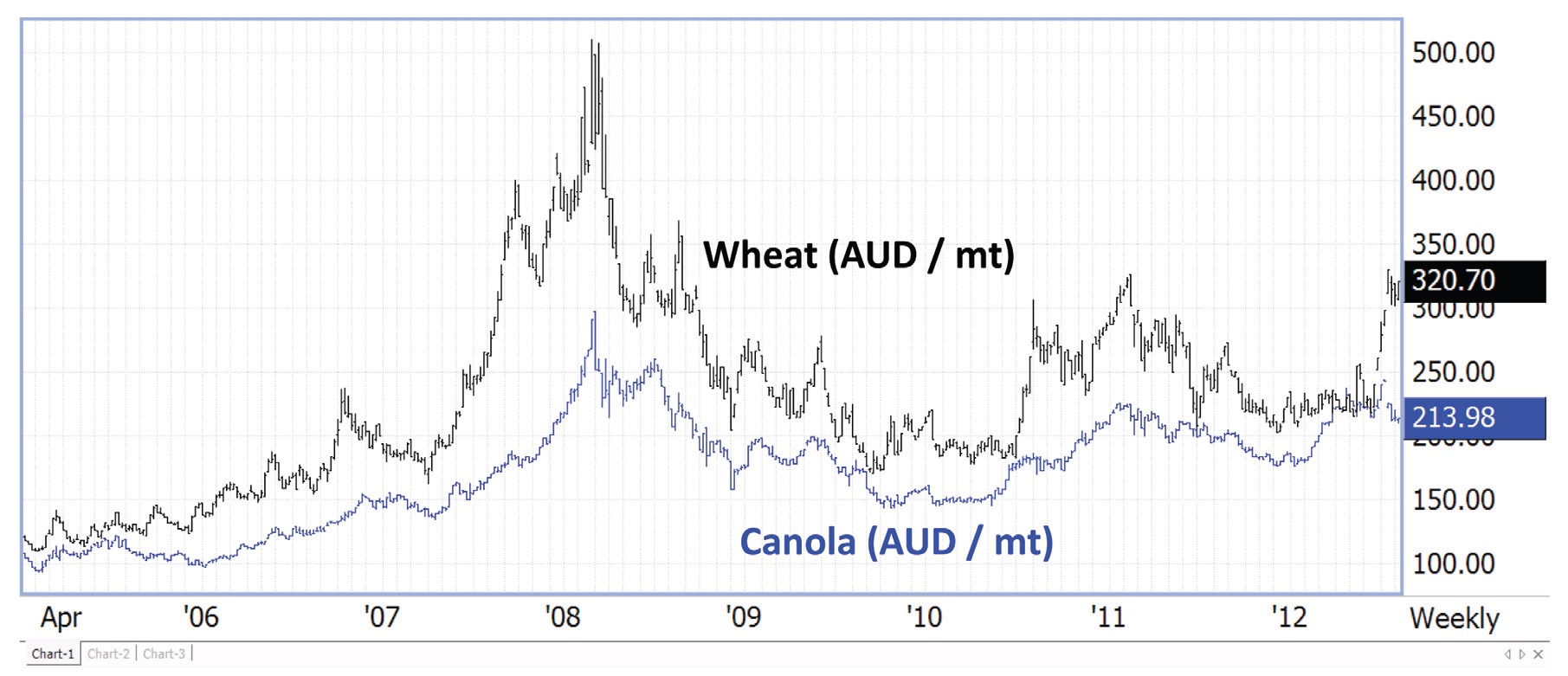

Figure 2. Recent canola and wheat price history (Data source: Future markets)

Corn – US crop cooked

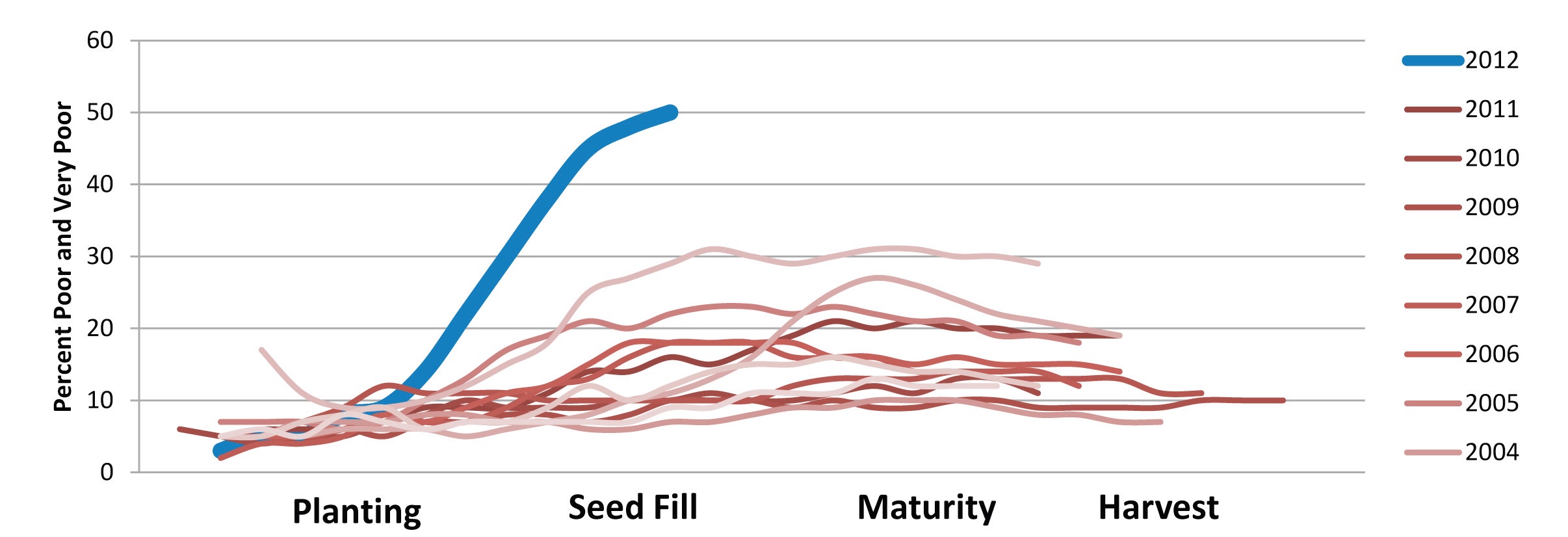

- US drought conditions in the last couple of months have driven corn conditions to the worst in years

- Harvested acreage expected to be diminished relative to record planting acreage due to failed crop areas.

Figure 3. US corn condition

Corn – Crop Predictions

- Yield predictions ranging as low as 117 bu/acre vs. early season USDA estimate of 166 bu/acre.

- Recent yield reports of 160 - 200 bu/acre on irrigated land in the south contrast with farmers chopping failed crops in the heart of the corn belt

Corn – Demand Revisions

- At 40% and 45% of domestic consumption, Feed and Ethanol use (respectively) are the top two drivers of demand for US corn

- Government mandates support ethanol as a driver of energy independence.

–Politically sensitive issue in election year as it has a direct impact on rural economies in key voting states

- Ethanol margins currently supported by high crude prices and demand for ethanol as a fuel oxygenate

- Livestock producers have been hit with drought impacts on pasture and hay lands, in addition to higher prices from reduced corn crop expectations

Soybeans

- Drought impacts in the US have so far not proved as severe as corn, due to later planting dates, but have been significant

–USDA currently 36.1bu/ac vs. 43.9bu/ac at the start of the year.

–Key reproductive period is coming up and the crop will be sensitive to rainfall in the coming weeks.

- Expected record plantings for 2012-13 South American crop as producers attempt to cash in on high prices.

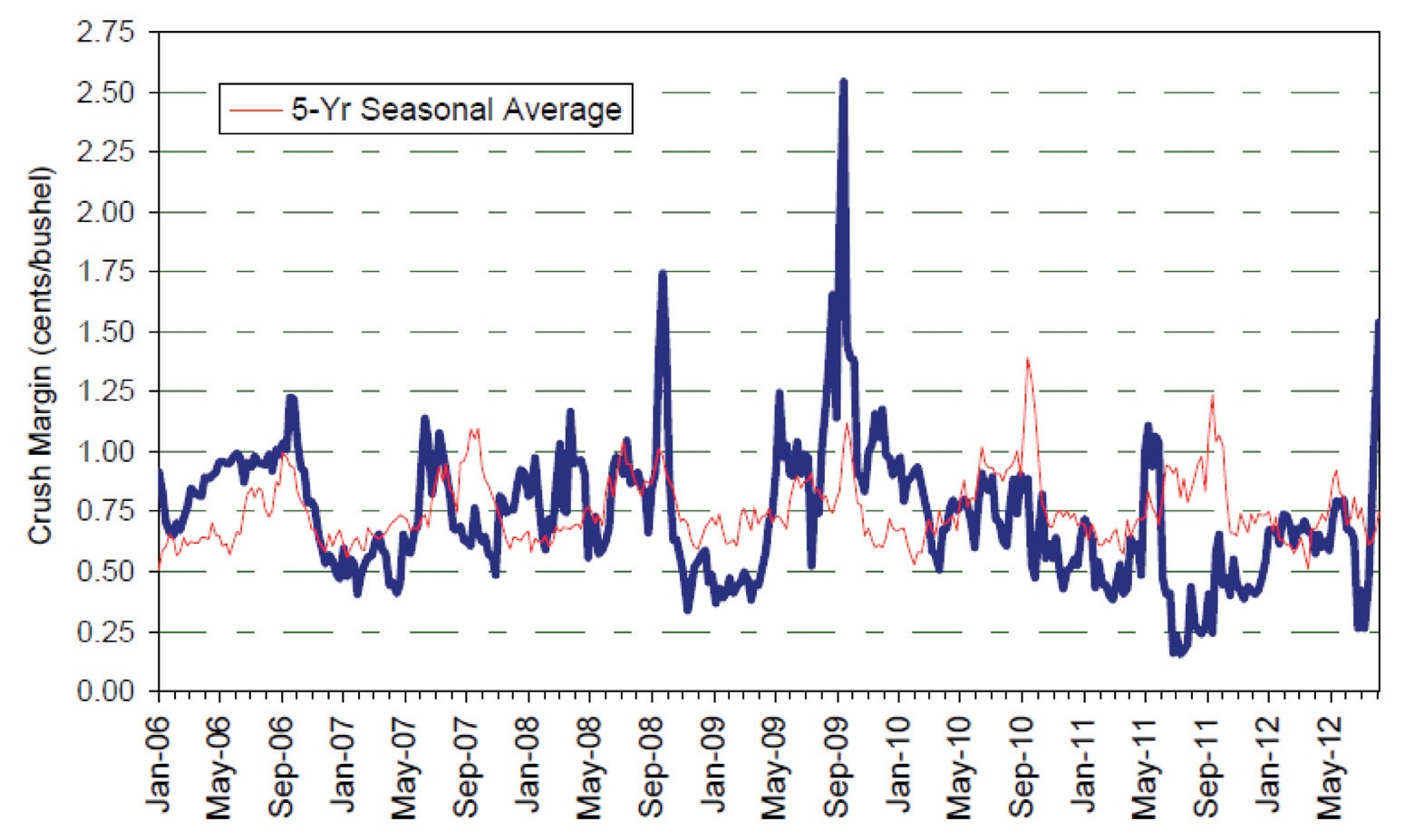

- Poor Chinese crush margins (on paper) contrast with reports of strong import demand due to government support on livestock prices.

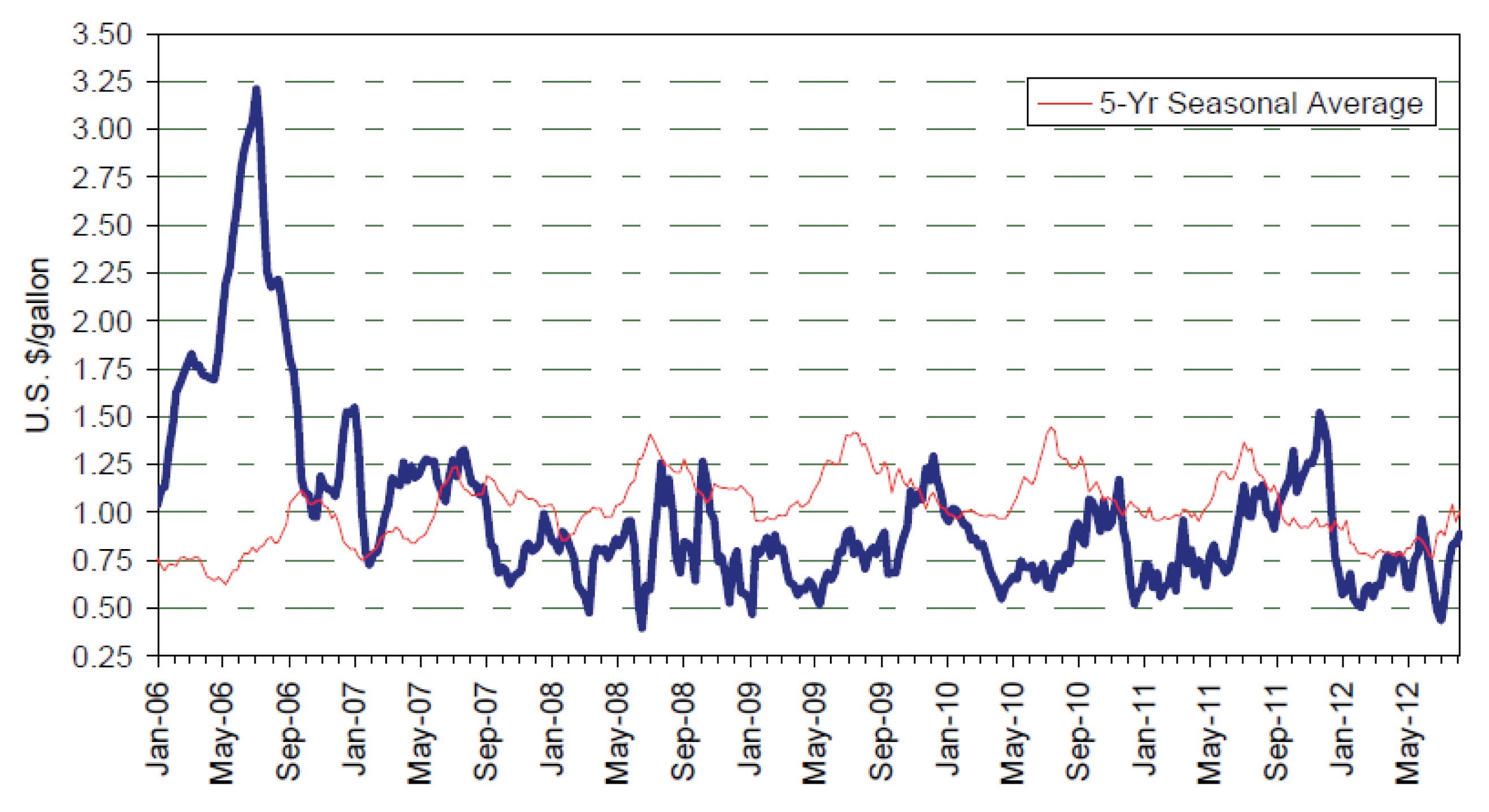

Figure 4. US soybean crush margin

Figure 5. US ethanol margin

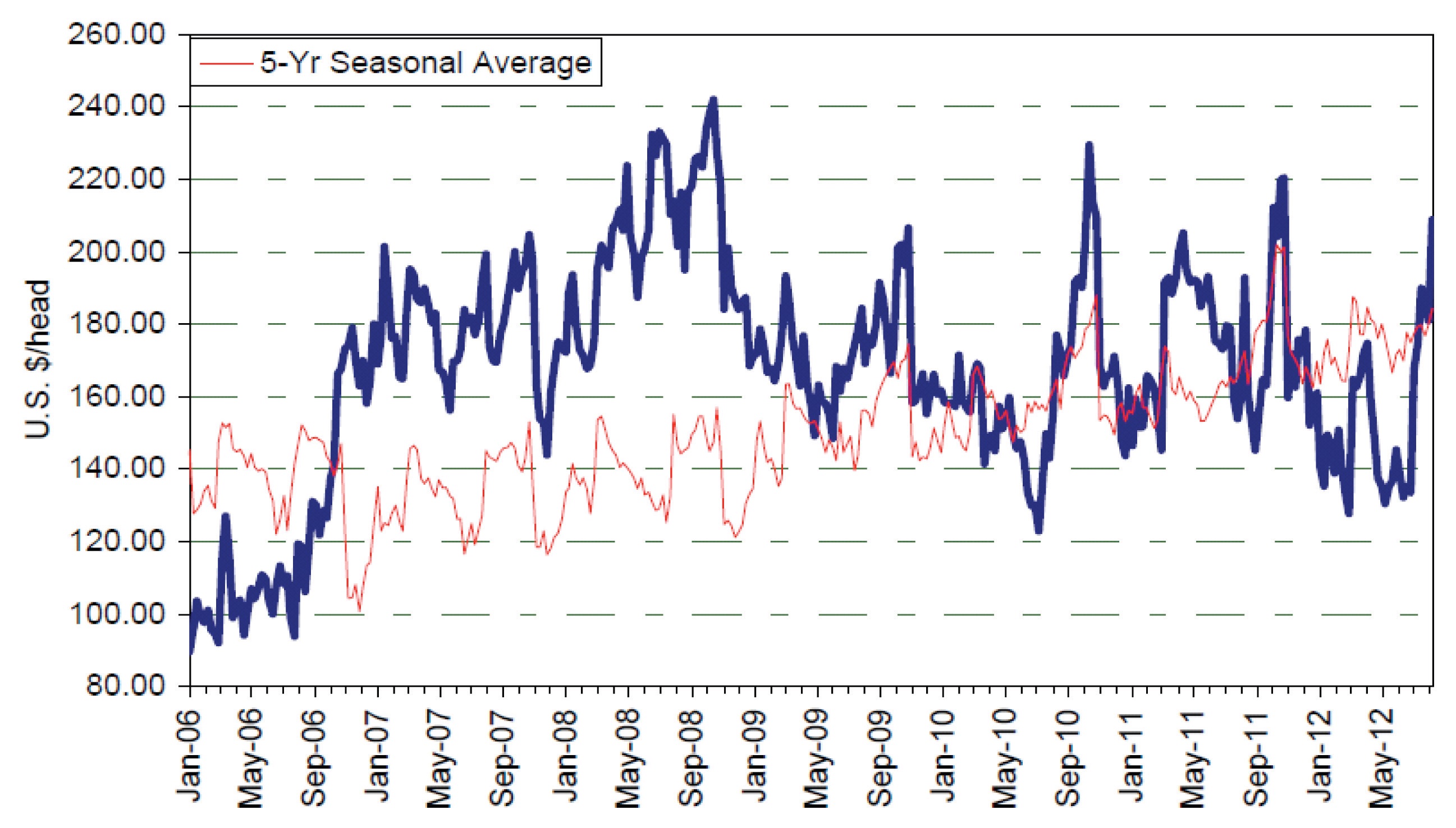

Figure 6. US feed cattle margin

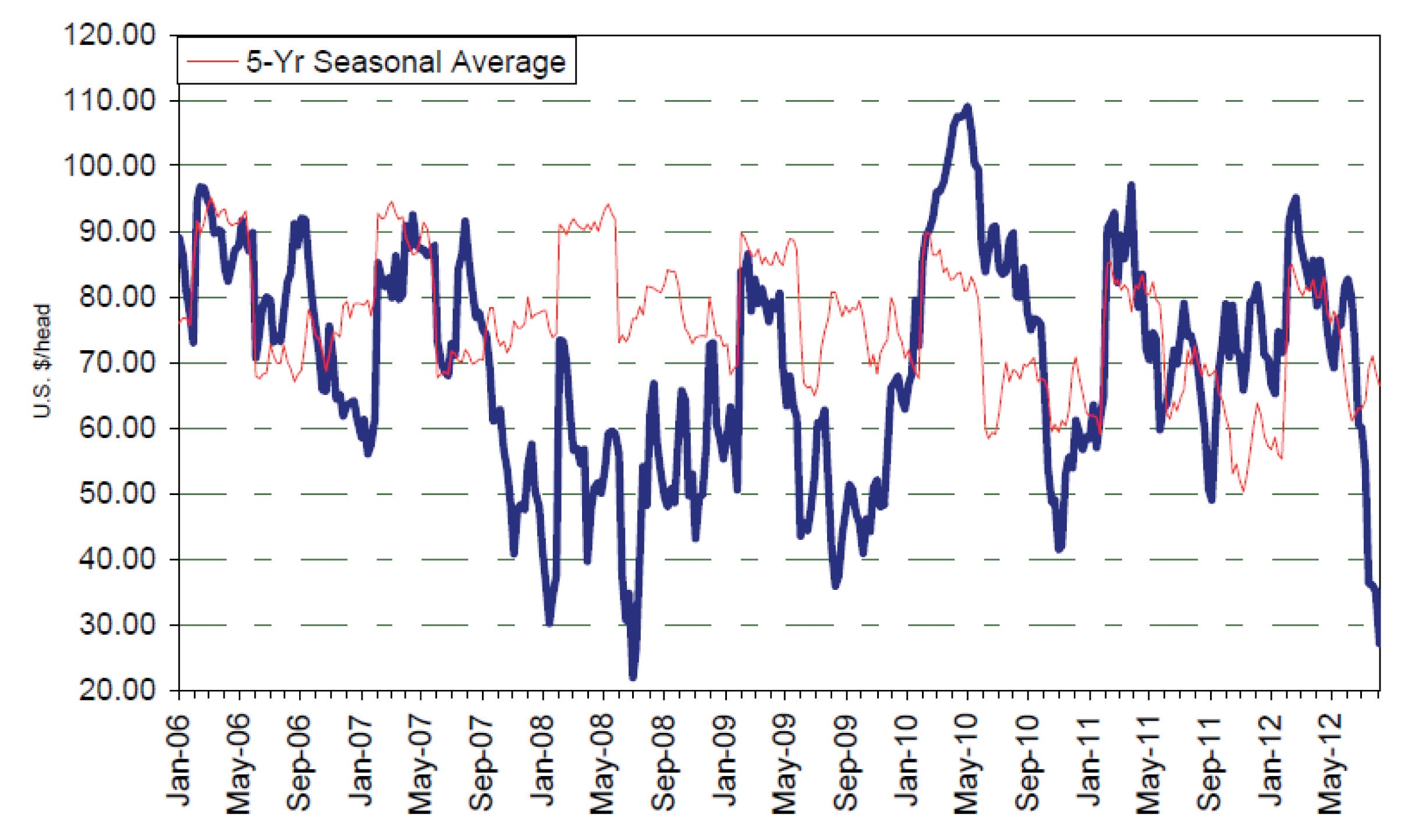

Figure 7. US hogs margin

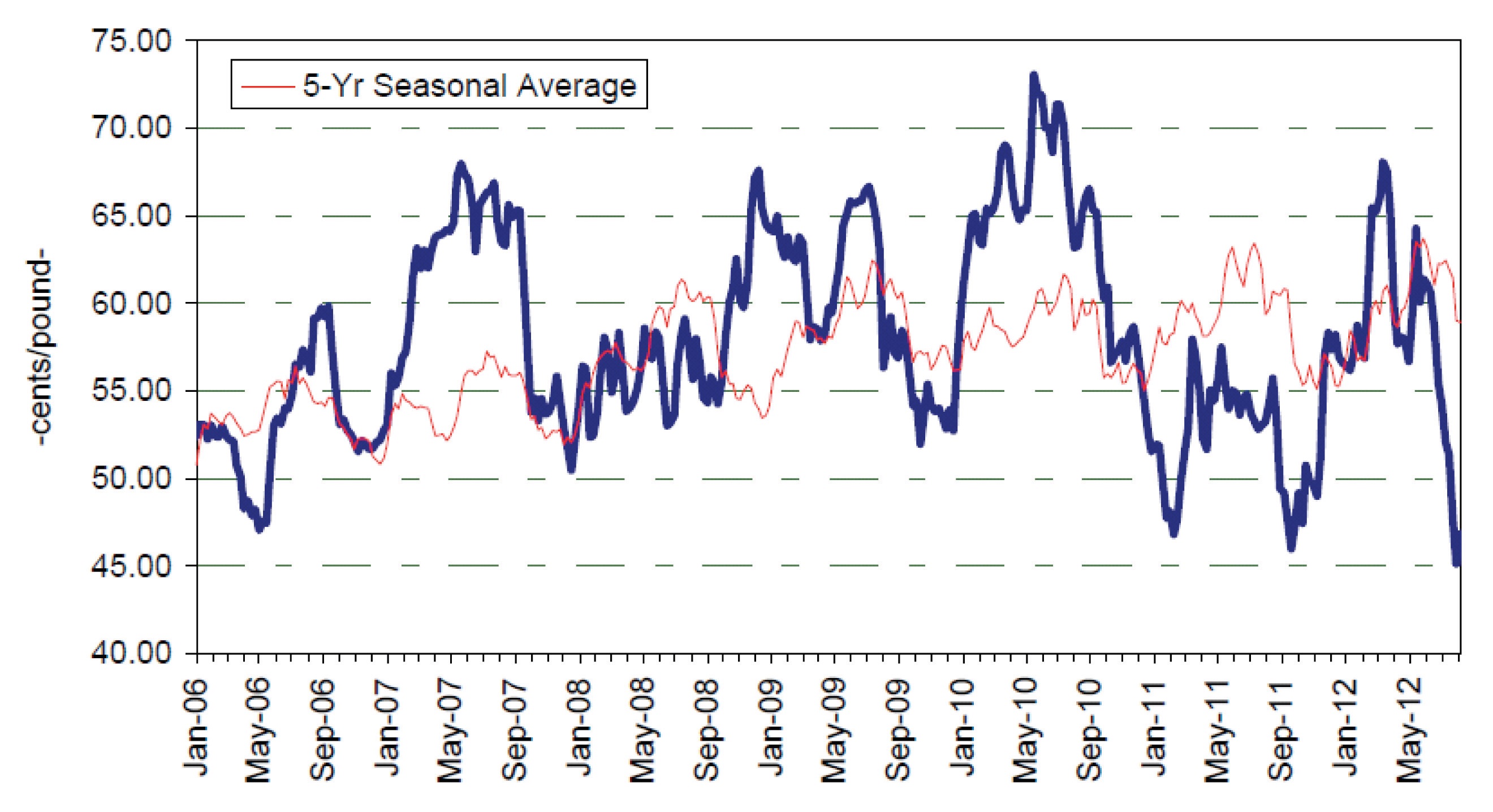

Figure 8. US broiler margin

Wheat

- Russian wheat crop currently in the middle of harvest, with drought impacts producing cuts in production forecasts, potentially approaching 40 mmt vs. 56 mmt last year.

–Speculation regarding possible export restrictions in 2013

- Slightly lowered Australian production estimates may restrict total wheat exports, talk of El Nino and drier WA weather patterns keeping market on watch.

- Wheat price supported by strong corn and soybean prices as feed consumers look to alternative sources.

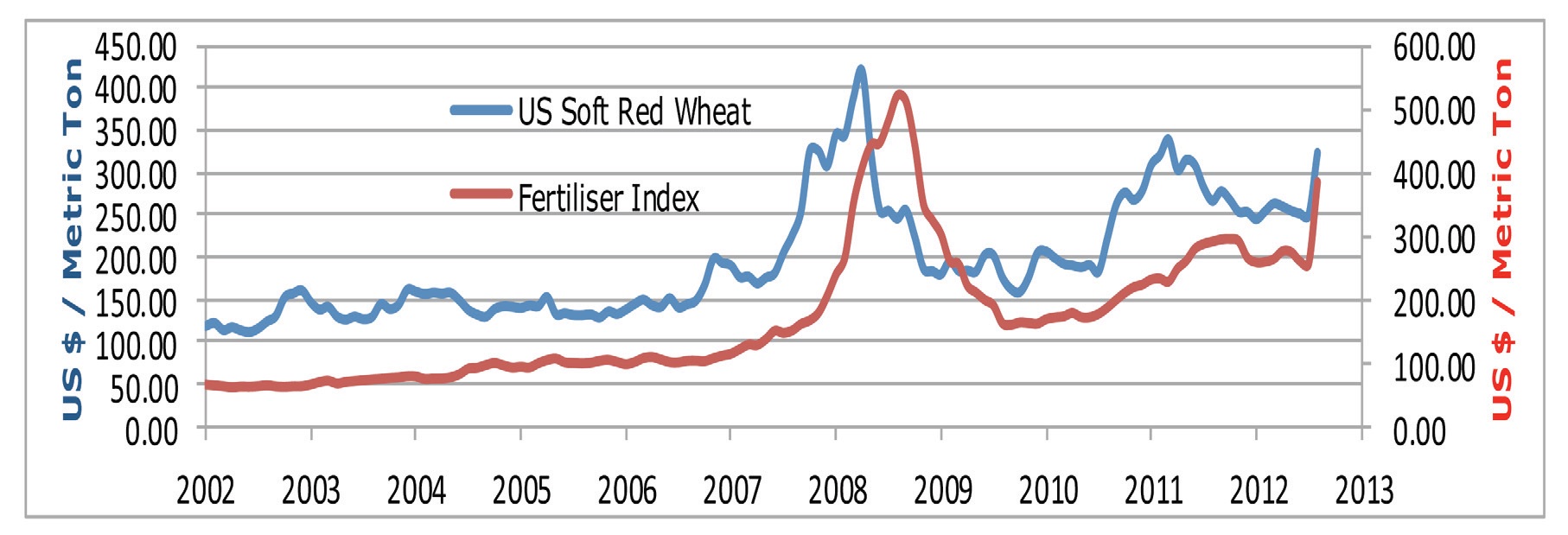

Fertilizer Outlook

- Jumps in commodity prices historically translate into increased fertilizer demand.

- Prices have firmed recently, but activity in the market has remained low. This may change as Australian consumption increases and South American crops get planted.

About Lachstock Consulting

- Providing a marketing plan that is tailored to each individual business

- Combine market and business analysis to create objective targets with a long-term approach.

- Focus on hedging and risk management; not crystal balling and speculation.

- Be more objective and less emotive.

- The marketing plan is complimented with real time position keeping, market information and over the phone advice.

- Focusing on Western Victoria, Riverina, and Southern Queensland.

Summary

- Final results of US drought will have a strong impact on the market

- Demand changes will be dependent on ultimate world supply

- A lot can and will change in the coming 12 month marketing window.

- Be objective and realistic about your targets.

- Measure Risk vs. Reward and only hedge when the risk and reward warrants it and don’t look a gift horse in the mouth.

- Be consistent with your plan and maintain a disciplined approach.

Contact details

Lachie Stevens

Lachstock Consulting

0419 305 519

Was this page helpful?

YOUR FEEDBACK